This figure applies the methodology like shown in "Fair Value DCF".

IFRS related requirements are linked to the following headlines:

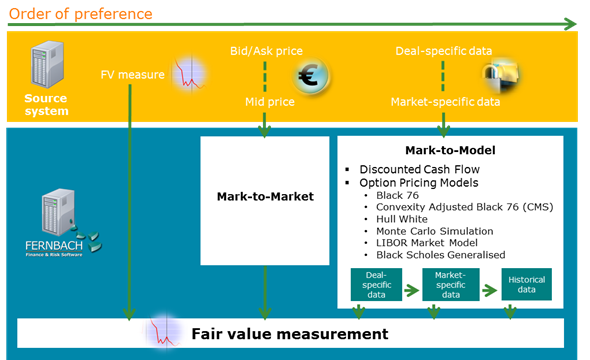

In order to be compliant with IFRS and take into consideration the IT circumstances of a bank, the solution uses the following ranking for fair value:

- Use of fair value measures that already exist in external systems, provided these figures are IFRS-compliant.

- Mark-to-market approach: Use of market prices as an input for the determination of fair value.

- Mark-to-model approach: If both points 1 and 2 are not available, the solution uses inputs from the market in the form of parameters.

Using this hierarchy, it is ensured that a valuation result is only calculated once and then used for all analysis systems according to the principle of “single calculation”.

1. External fair value measurement:

If fair value measures have already been calculated outside the solution, these figures could be delivered to the solution as an input, provided these figures are IFRS-compliant. Alternatively, it is possible to manually capture the valuation results for a financial instrument in web-based dialogues. In order to fulfil requirements for accounting and reporting purposes, the solution expects external systems to deliver fair value ratios at a certain level. For example, the solution expects the decomposition of fair value changes in view of changes in market rates, changes in credit spread, amortisation and accrued interest-related parts. In addition, if a bank designates a hedge relationship between deals, the solution would expect ratios such as Hedge EIR to be delivered in order to improve the quality of effectiveness testing. Please note that for the delivery of external fair value measures, the solution will not calculate these fair value figures again.

If no external FV measure is provided, the solution will calculate fair value figures either through a mark-to-market or a mark-to-model approach.

2. Mark-to-market approach:

Within the mark-to-market approach, the solution uses quoted prices in an active market as a first priority. The solution expects that the bid price will be delivered for assets held or liabilities to be issued and that the asking price (sometimes referred to as “current offer price”) will be delivered for an asset to be acquired or liabilities held. If no current market price is available, an entity can deliver a historical price to the solution, provided no significant changes in economic circumstances have occurred. The historical price should be adjusted in case conditions have changed. The solution has experiences in connecting to different market information providers and in using appropriate market prices for fair valuing.

3. Mark-to-model approach:

If there is no active market or if markets have become inactive, the market price can not be considered as the fair value. In this case, an entity can measure fair value by using a valuation technique. A valuation technique would be expected to arrive at a realistic estimate of fair value if

- it reasonably reflects how the market could be expected to price the instrument and

- the input to the valuation technique reasonably represents market expectations and measures of risk-return factors inherent in the financial instrument.

The solution provides advanced mark-to-model valuation techniques, including but not limited to

- discounted cash flow method,

- option pricing formulas and

- Monte Carlo simulation.

These models are commonly used by market participants to price the related financial instruments. For all these models, the solution makes maximum use of market inputs and relies less on entity-specific inputs.