Highlights of the blueprint:

|

The IFRS 9 valuation blueprint covers the entire functionality that is necessary to deal with the valuation requirements specific to IFRS 9 with regard to initial and subsequent measurement. It contains several components that generate estimated cash flows while taking several types of information such as contractual data, market rate sources and customer payment behaviour into account for the prediction of the future cash flow plan. Regardless of whether the estimated cash flow plan is generated by the solution or if is delivered by another source, components such as EIR calculation or fair value calculation produce the necessary valuation elements related to Amortised Cost (AC) and Fair Value (FV). As such, valuation elements are provided on a highly granular level, offering great analysing options based on a combination of granular valuation elements and descriptive deal data.

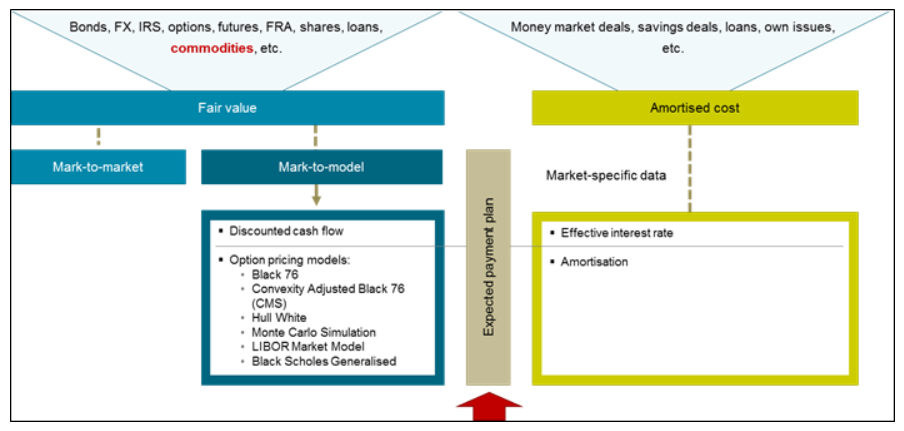

In general, IFRS9 calls for an entity to measure its financial instruments on the basis of amortised cost (AC) or fair value (FV), depending on the accounting category assigned.

There are different ways to calculate AC and FV for a deal:

For all approaches, the estimated future cash flow plan of a deal forms the basis for the calculation.

In the case of fair value calculations, the mark-to-model approach uses the discounted cash flow method for calculation.

For amortised cost calulations, the effective interest rate (EIR) is needed. According to IFRS9, "when calculating the effective interest rate, an entity shall estimate the estimated cash flows

- by considering all the contractual terms of the financial instrument (for example: prepayment, extension, call and similar options)

- but shall not consider the expected credit losses.”

The blueprint valuation consists of the following groups of components:

Cash flow generation

For details about cash flow generation, please refer to Core Cash Flow Generation

- Initial and subsequent measurement

For details about initial and subsequent measurment, please refer to Core Valuation

IFRS 9 valuation requirements can be split into the following functions:

- Cash Flow Plan Generation

- Effective Interest Rate Calculation

- Amortised Cost Calculation

- Fair Value Calculation

- Impairment Adjustment Calculation