In the section "Core Valuation: Effective Interest Rate" the mathematical formular, challenges in calculation as well as the splitting of the EIR in various elements is explained in general.

...

By detecting a change in the contractual deal data that are delivered, the solution automatically triggers a recalculation of the EIR and/or adjustment of the amortisation plan according to IFRS9, including but not limited to:

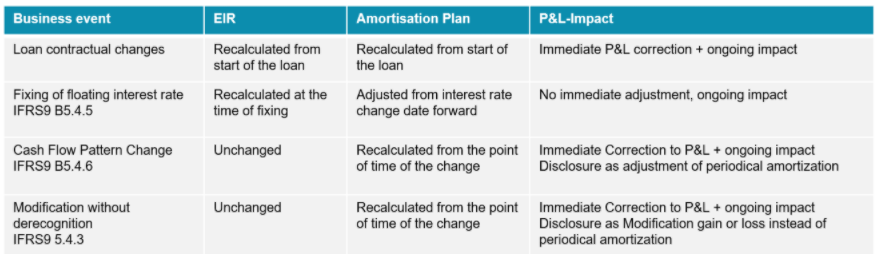

For IFRS, the impact of changes in deal data are considered like following:

...

| Expand | ||

|---|---|---|

| ||

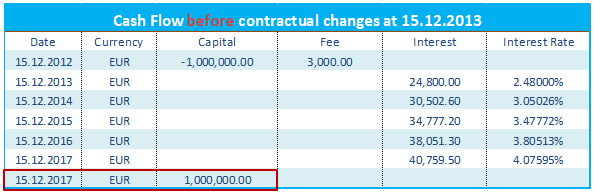

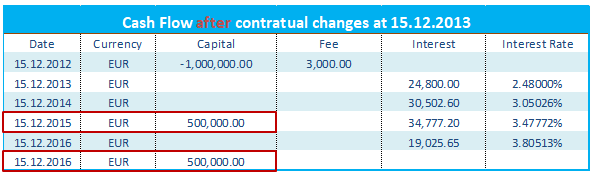

Scenario: The contractual payment plan for a loan is restructured. For example, let us consider that the original cash flow plan for a deal is as follows:

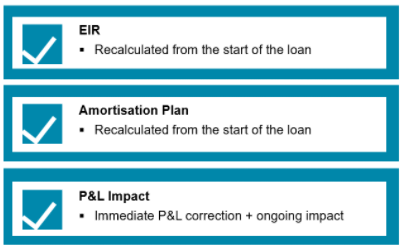

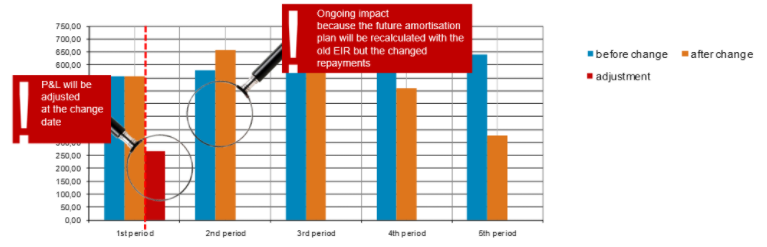

The impacts of this change on the EIR, the amortisation plan and the P&L are as follows:

The effects on the amortisation of the fee are as follows:

|

| Expand | ||

|---|---|---|

| ||

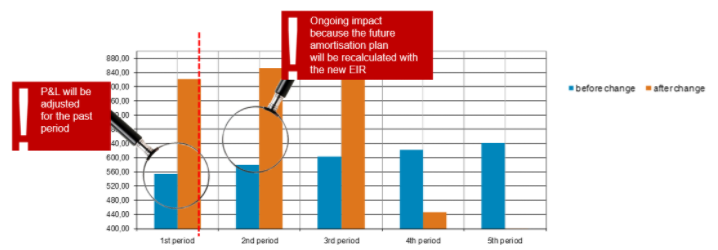

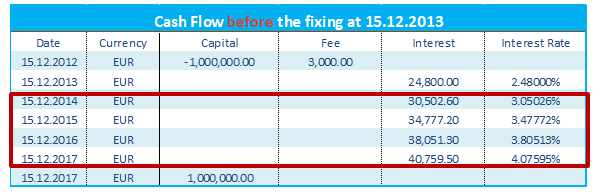

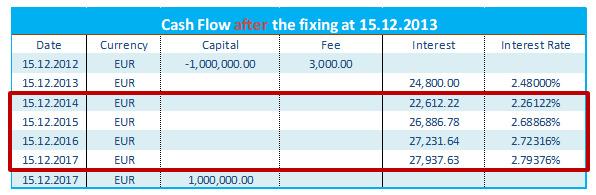

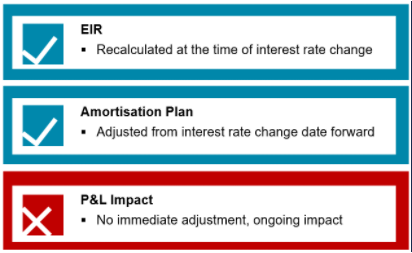

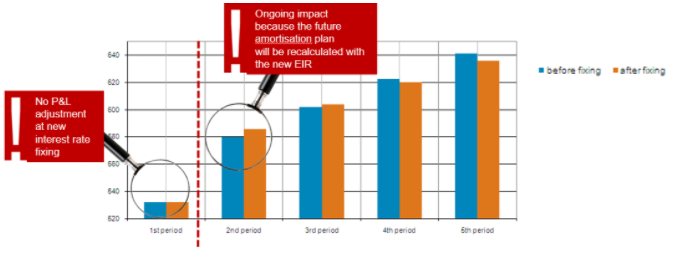

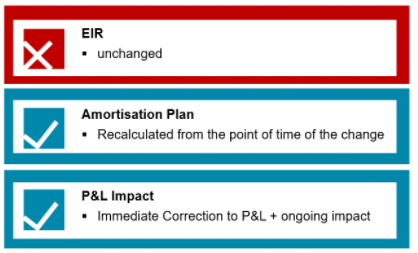

Scenario: Changes in interest cash flows for a floating deal (the interest rate of the deal is reset). IFRS9 has specific requirements for this scenario: In the case of a financial instrument with a floating interest rate, the EIR should be periodically adjusted to reflect the latest market conditions in accordance with IFRS9 B5.4.5. The recalculation of the EIR has no immediate impact on profit and loss but the future amortisation plan should be adjusted on the basis of the revised EIR. For example, let us consider that the original cash flow plan for a deal is as follows:

The impacts of this change on the EIR, the amortisation plan and the P&L are as follows:

The effects on the amortisation of the fee are as follows:

|

| Expand | ||

|---|---|---|

| ||

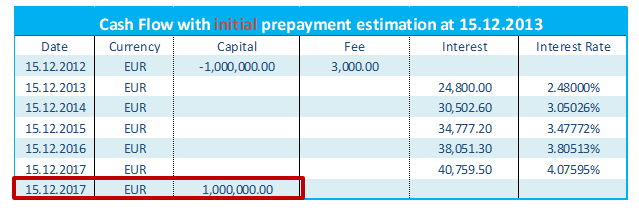

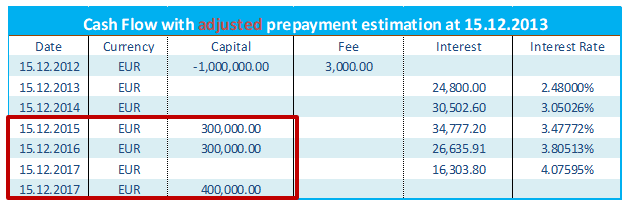

Scenario: The expected future cash flows change. For example, let us consider that the original cash flow plan for a deal is as follows

The impacts of this change on the EIR, the amortisation plan and the P&L are as follows:

The effects on the amortisation of the fee are as follows:

|

| Expand | ||

|---|---|---|

| ||

The term "modification" in accordance with IFRS9.5.4.3 relates to adjustments to the contractual cash flows for financial assets. A modification is an adaptation of the terms of the contract, whereby the nature and scope of a modification determines the accounting consequences. A modification can occur due to various reasons including but not limited to a customer's financial difficulties. The following modifications to contractual agreements might have an impact on the estimated cash flow plan. They need to be considered as “Modification” in the solution:

The following cases are not to be considered as “modification of contractual data” within the scope of IFRS 9.5.4.3:

By means of a contract modification, a substantial change in the contractual components may lead to a derecognition of a financial asset and thus to a corresponding recording of a "new" financial asset or, on the other hand, to a continuation of the previous financial asset in so far as the deal has not substantially changed. When moving from IAS 39 to IFRS 9, for “renegotiation or modification”, a “clearer” guideline has been provided for the modification of contractual terms.

If there is no derecognition of the financial asset as a result of the contract modification, the adjustment of the carrying value of the financial asset as a result of the modification is recognised as a modification gain or loss in profit or loss. The amount of this book value adjustment and the resultant modification result is determined as the difference between the book value of the modification and the modified contractual payment flows discounted with the original EIR. |

...