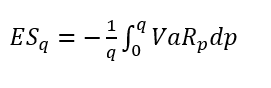

The Conditional Value at Risk (CVaR), also referred to as Expected Shortfall (ES), is used to disclose the average expected loss on a portfolio for probability q that can occur within time horizon t. A 1-day-5%-ES of 10 million euros means that the average loss for the portfolio in the worst 5% of all possible cases that can occur in one day is 10 million euros. The ES is an average over all VaRs at different confidence levels. The formal definition of the q%-ES is:

Portfolios can be defined freely using business criteria such as deal type, bank segment or organisation unit. Please see Value at Risk (VaR) for more information on Value at Risk (VaR). The interest rates, volatilities and correlations, required by the approach that is used, can be imported via the import of market data.