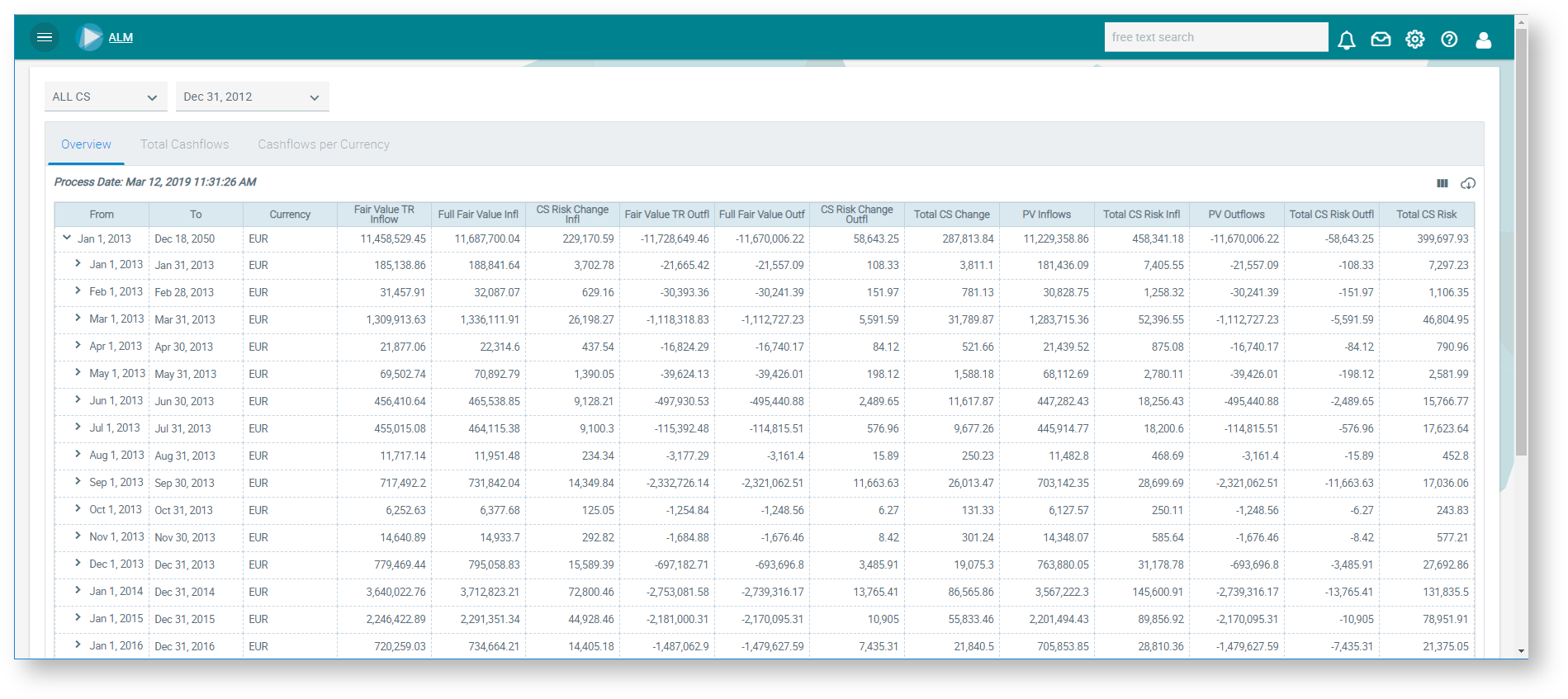

The impact of the credit spread on the fair value (full fair value and fair value with constant credit spread) of a portfolio such as the banking or trading book is shown. Credit spreads can be delivered using the market data for each posting date or alternatively, they can be determined from the probability of default (PD) and the loss given default (LGD).

The credit spread risk is determined with the help of the credit spread on the deal conclusion date and the current posting date. The credit spreads are added to the interest rates when the discount factors are determined. The interest rates for the posting date are always used so that the difference between these discount factors reflect the credit spread. The cash flows discounted by these discount factors are displayed for each period in a freely definable period grouping. The cumulative credit spread risk is then determined as the sum for each period.