FlexFinance provides data marts that contain information required for credit risk management. This information has been called for by the BCBS (= Basel Committee on Banking Supervision) in order to define capital requirements.

The procedure to calculate credit risk according to BCBS guidelines overlaps with that for the calculation of risk provisions according to IFRS in many cases.

The data marts contain all the information required to differentiate between financial products and counterparties as well as all the individual components needed for reporting purposes or credit risk management.

- Calculated results

- RWA (Risk-weighted assets)

- PD (Probability of Default)

- LgD (Loss Given Default)

- CF (Conversion Factor) products with drawing risks

- FX haircut

- Maturity mismatch

- Hc (coll) or Hc (claim) haircut for collateral or claim

- Correlation

FlexFinance allows parallel calculations to be made in accordance with various regulatory approaches (standard, IRB, CAD), the use of which for reporting purposes has to be approved by the national authorities in each case.

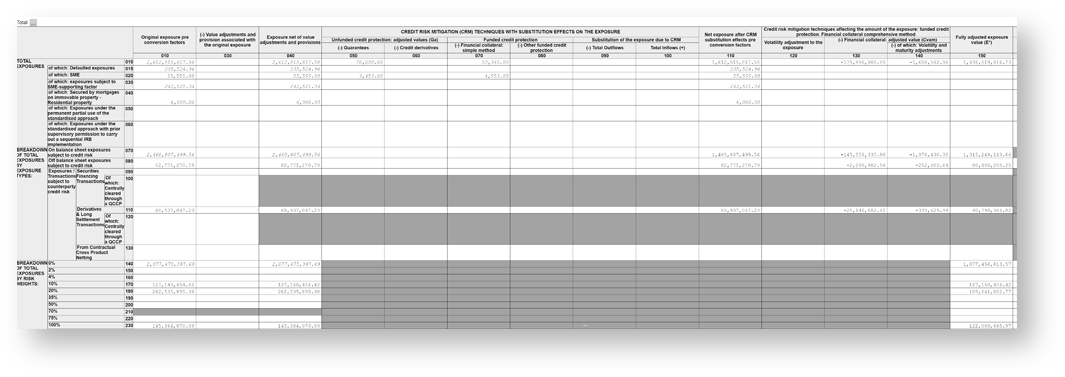

Below is an example of a credit risk report in FlexFinance based on these data marts:

The following standard functions are also available for reports defined in FlexFinance:

- extensive drilldown possibilities

- possibility to compare the report for different posting days

- proof of rule for reporting contents

- manual editing combined with consistency check