The contractual elements of a loan agreement are represented in the software via various modules. Each of these modules provides a portfolio of functions that are used depending on product-specific requirements.

The modular design ensures that the solution can be used as a single pane of glass for all loan types. Its spectrum ranges from simple universal loans over real estate loans to complex corporate loans and project financing.

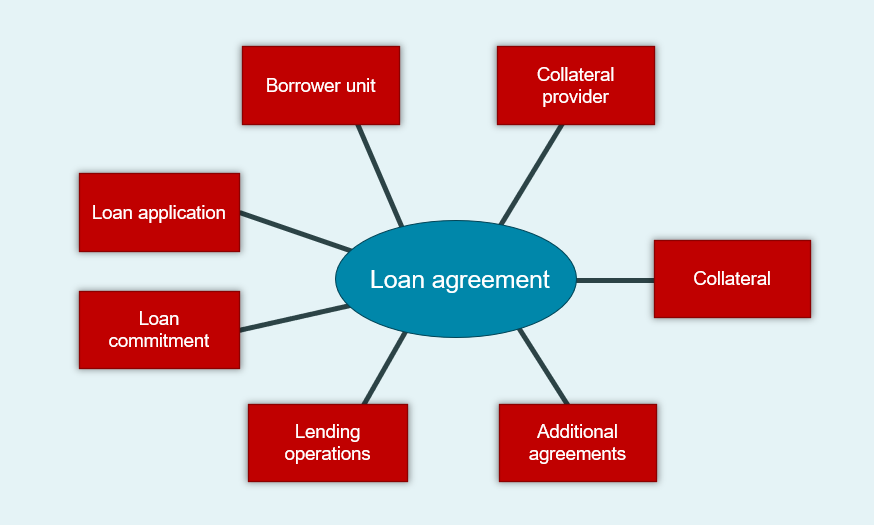

Loan agreement

The “Loan Agreement” module contains the contractual agreements of a loan. They determine the following aspects of a loan:

- the borrower unit

- the lending operation with its payment plan based on the contractual terms as well as the payment monitoring

- the collateral with the respective collateral provider

- the additional agreements

From a timeline perspective, a loan agreement has different phases that need to be considered separately:

- loan application

- loan commitment

- loan agreement

In order for a loan agreement to be legally effective, a loan application by the borrower unit, a loan commitment by the bank and an acceptance of the commitment by the applicant are always required. Only after a positive loan decision by the bank and acceptance of the bank’s loan offer by the borrower unit, the loan agreement is concluded.

Depending on the specific loan product, this process can be individually customised in the software to the respective requirements. Customisation ranges from changing the responsibility of a role in the approval process to merging different steps. For retail deals, e.g., a binding offer can already be presented directly while recording the financing request. The loan agreement is then concluded based on highly standardised conditions the moment the financing request is submitted.

Loan application

The loan application is submitted by the borrower unit and generally describes the respective financing requirements. In the context of the loan application, information of the borrower unit that is relevant to the bank’s application review is also collected. Collateral data is collected as well.

The solution supports the collection of a comprehensive data set for a well-founded loan decision. The loan application can be recorded on-site in a branch office or online by the customers themselves. In addition to the traditional online recording process via a wizard, a chatbot is also available.

Loan commitment

The loan commitment is the last step of the approval process. The approval process includes the assessment of creditworthiness and capturing and valuating collateral.

Commitments can be made bindingly or revocably. This has an impact not only on the outpayment obligations of the bank, but also on risk provisions and accounting.

The loan commitment makes the loan agreement legally binding.

In the software, multiple lending operations can result from a single loan commitment. Or, in other words: A loan agreement can include multiple lending operations. Whether or not a loan commitment results in multiple lending operations depends on the complexity of the product. If several outpayments are foreseen for a loan agreement, each with separate repayment and interest terms, it is advisable to map a separate lending operation for each outpayment within the framework of a joint loan commitment/agreement. If several outpayment dates are foreseen, which just act like capital increases under the same conditions, the loan agreement can be mapped as a single lending operation. This also applies if the conditions change over time, but these changes do not have to be split proportionally between historical outpayments.

Borrower unit

Each loan agreement is mapped to exactly one borrower unit.

However, a borrower unit can have more than one loan agreement.

A borrower unit can be a single borrower or consist of multiple borrowers. Any legally independent entity – individuals, project companies, corporations and entities with other legal forms – can be a borrower.

An individual borrower can

- be assigned to different borrower units,

- in addition to the assignment to a borrower unit, be part of an economic unit,

- and optionally be a collateral provider.

In addition, “economically entitled persons” in the sense of the Money Laundering Act can be assigned to borrowers.

Lending operation with payment plan and payment monitoring

A lending operation is always assigned to a single borrower unit.

However, several items of collateral can be assigned to the lending operation.

Payment plan

The lending operation generally comprises the contractual agreements for the specific deal, the resulting payment plan, as well as the payment monitoring and thus the payment management.

Based on the contractual agreements in the loan agreement, the software supports transactions including, but not limited to:

- individual, multiple outpayments

- flexible due dates for repayments and interest payments

- annuities, fixed repayments

- fixed and variable interest rates

Loan management

The software supports many types of business transactions that change the loan agreement during its term. These transactions resulting in adjustments to the payment plan during the term of the lending operation include, but are not limited to:

- change of due date, term, payment dates

- deferral, suspension, capital increase, special repayment, interest adjustment

- forbearance measures, which optionally lead to a qualification of the receivables as “forborne exposure”, and whose recovery periods are monitored

Payment management

The software’s payment management features include setting of due dates and the monitoring of payments. Based on payment routes, incoming and outgoing payments are generated and transferred to a payment system.

Due dates and payments are posted in the “Loan” sub-ledger, but can optionally be posted in the general ledger, too.

Expected incoming payments are monitored, overdue payments are identified and days past due are calculated.

Taking into account the product, the days past due as well as qualitative criteria of the borrower unit, a dunning level that can be defined individually is assigned to the deal. Various dunning actions can be triggered for each dunning level.

Collateral

An item of collateral can be legally assigned to several lending operations in the loan agreement (“Assignment”).

The solution supports several types of collateral:

1. Personal collateral:

- Guarantees

- Suretyships

2. Physical collateral:

- Pledges

- Transfers of collateral

- Charge by way of legal mortgage

For all lending operations for which collateral may generally be used, the current value of the collateral is allocated. There are two supported methods for allocating an item of collateral to several loans: “Rank” and “Value”. With the “Rank” method, on the reference date, the value of the collateral is successively allocated to the assigned loans depending on the rank of these loans, and with the “Value” method, each loan is allocated a fixed amount of the collateral value.

The following information can be recorded for collateral:

- Object information depending on the type of collateral

- Lending value

- Automatic haircut, manual safety deduction

- Person/role responsible for collateral valuation, periodicity and monitoring of re-assessments

Collateral provider

The collateral provider can, but does not have to, belong to the borrower unit.

Additional agreements

The solution supports the recording and monitoring of contractual clauses or additional agreements that are not directly related to the payment plan of a lending operation.

Additional agreements can be added to the loan agreement. If compliance needs to be checked regularly, follow-ups can be set up, notes can be entered and documents can be uploaded.

Thus, for example, a commitment by the borrower unit can be implemented to regularly provide information, e.g. by means of quarterly reports, or a commitment to comply with defined financial requirements can be monitored and documented, e.g. regarding the maximum debt as measured using the leverage ratio.

If necessary, the additional agreements can be suspended and a fee can be charged for the suspension.

Infrastructure

The “Loans” module can be integrated into any technical and organisational infrastructure.

Configurations are carried out on a “product” basis. Processes are modelled via workflows.

Optionally, postings for the balance sheet and the P&L account can be generated for the “Loans” sub-ledger. This also includes the calculation of an IFRS 9 compliant risk provision as well as the provision of data sets on an individual deal level for the preparation of EBA-FINREPs.